Hiện nay, hồ sơ lập ủy quyền quyết toán thuế dành cho cá nhân thuộc các trường hợp được tổ chức, cá nhân trả thu nhập quyết toán thay bao gồm mẫu số 02/UQ-QTT-TNCN ban hành kèm theo Thông tư 92/2015/TT-BTC (Xem thêm các trường hợp được ủy quyền quyết toán tại https://gonnapass.com/cac-truong-hop-duoc-uy-quyen-quyet-toan-thue-tncn/)

Vậy trong một số trường hợp, doanh nghiệp có nhiều cá nhân thuộc trường hợp được ủy quyền quyết toán thuế TNCN, việc lập ủy quyền quyết toán thuế thông qua phần mềm cho nhiều lao động liệu có được chấp nhận?

Được lập uỷ quyền quyết toán thuế TNCN qua phần mềm quản lý nhân sự

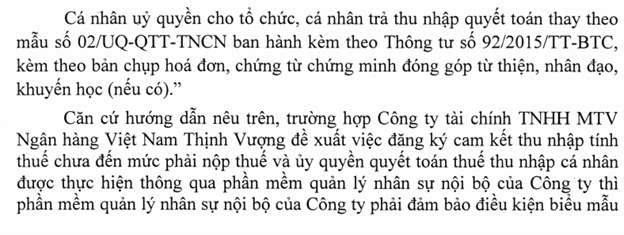

Quan điểm của Tổng cục Thuế tại công văn số 3363/TCT-DNNCN ngày 17 tháng 8 năm 2020 đưa ra ý kiến chấp nhận cho doanh nghiệp có thể lập ủy quyền quyết toán thuế TNCN thông qua phần mềm quản lý nhân sự nội bộ với điều kiện biểu mẫu đáp ứng đầy đủ nội dung theo mẫu số 02/UQ-QTT-TNCN đã quy định.

Có thể thấy, hướng dẫn này hợp lý và tạo thuận tiện cho việc quản lý của doanh nghiệp đặc biệt với những doanh nghiệp quy mô lớn với nhiều lao động.

Tham khảo công văn:

Công văn 3363/TCT-DNNCN ngày 17/8/2020

Căn cứ luật:

Trích dẫn Điểm a.4, Khoản 3, Điều 21, Thông tư 92/2015/TT-BTC

Tham khảo video

According to Clause 1, Article 21, Circular 92/2015 / TT-BTC:

“a.3) Payers of taxable wages shall declare PIT on behalf of wage earners and make annual statement of PIT if authorized by wage earners, whether tax is deducted or not.

Dossiers of authorization for tax finalization of individuals for organizations or individuals paid income include:

– Form No. 02 / UQ-QTT-TNCN attached to Circular 92/2015 / TT-BTC

– Copies of invoices and documents proving charitable, humanitarian and study promotion contributions (if any)

In some cases, if the company has many individuals authorized to finalize PIT, is it acceptable to establish an authorization to settle tax through software for many employees?

According to the General Department of Taxation’s response to the Ho Chi Minh City Tax Department in Official Letter No. 3363 / TCT-DNNCN dated August 17, 2020 providing an acceptable opinion for enterprises to establish an authorization for PIT finalization through internal human resource management software provided that the form fully meets the content according to the form No. 02 / UQ-QTT-TNCN specified. This is completely reasonable and facilitates the management of enterprises, especially large-scale enterprises with many employees.

However, businesses need to know clearly the regulations for the cases in which individuals are authorized to make PIT finalization for organizations or individuals paying for the finalization on behalf of. Specifically, at Point a.4, Clause 3, Article 21, Circular 92/2015 / TT-BTC has the following provisions.

Biên soạn: Trần Thị Lan Anh – Tư vấn viên

Bản tin này chỉ mang tính chất tham khảo, không phải ý kiến tư vấn cụ thể cho bất kì trường hợp nào.

Để biết thêm thông tin cụ thể, xin vui lòng liên hệ với các chuyên viên tư vấn.

Đăng kí để nhận bản tin từ Gonnapass